Why Buying Options Feels Unfair: The Brutal Truth About Time Decay

Published: January 25, 2026

Tags: theta, decay, buying, options, time, decay, extrinsic, value

Have you ever nailed the direction of a stock move perfectly—only to watch your option trade end up flat or even in the red? You're not alone. Many new (and even experienced) traders discover the hard way that being right on the stock isn't enough when you're buying options. You need the move to be big enough and fast enough to overcome a silent killer: time decay.

In this post, we'll break down a classic example that illustrates exactly why option buying is so challenging, even when your market prediction is spot-on.

The Scenario: A "Perfect" Prediction That Goes Nowhere

Imagine a stock—let's call it YYYZ—trading at around $29. You're bullish and decide to buy a 30-day call option with a $30 strike price for $1.00 premium.

The option is slightly out-of-the-money (OTM).

Its entire $1.00 premium is extrinsic value (also called time premium)—there's no intrinsic value yet because the stock is below the strike.

Fast-forward to expiration: the stock has climbed to $31, exactly as you hoped.

At expiration:

Intrinsic value = $31 - $30 = $1.00

Extrinsic value = $0 (no time left)

Option worth exactly $1.00

You sell (or it settles) for what you paid: breakeven. No profit, despite correctly calling a ~7% move in the stock.

Now imagine the same $2 move ($29 → $31) happens much earlier—say, within the first week. With 23 days still left until expiration, the option would likely be worth far more than $1.00. You'd have significant remaining time premium on top of the $1.00 intrinsic value, potentially letting you sell for $1.80–$2.50 or more (depending on volatility). That's a solid profit.

The difference? Timing.

What Is Time Premium, and Why Does It Matter?

When you buy an option, you're paying for two things:

Intrinsic value (if any): The immediate "in-the-money" amount (stock price minus strike for calls).

Extrinsic value (time premium): The extra amount you're paying for the possibility that the stock moves favorably before expiration.

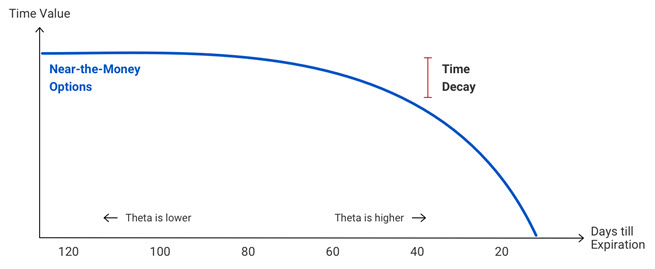

Extrinsic value exists because time gives the underlying stock more opportunity to make a big move. But here's the catch: as time passes, that opportunity shrinks—so extrinsic value steadily erodes toward zero. This erosion is known as time decay or theta.

Option buyers are effectively "renting" time. Every day that passes without a sufficient move chips away at your position—even if the stock price doesn't change at all.

Theta: The Option Buyer's Worst Enemy

Theta is one of the "Greeks" that measures how much an option's price is expected to decrease per day due to time passing (all else equal). For long options:

Theta is negative—time works against you.

Decay isn't linear: it accelerates dramatically in the final weeks and days before expiration.

In our example, the slow grind from $29 to $31 over 30 days let theta eat away the entire $1.00 extrinsic premium. By expiration, only the intrinsic value remained—just enough to get you back to even.

A faster move preserves some of that time premium, letting you capture profit before decay takes its full toll.

Why Is It So Hard to Make Money Buying Options?

The textbook highlights it perfectly: "It is not easy to make money when buying options."

To profit as an option buyer, three things generally need to align:

Direction: You have to be right (or mostly right) on the stock's move.

Magnitude: The move has to be large enough to cover the premium you paid (including overcoming the initial extrinsic value).

Speed: The move has to happen quickly enough to outpace theta decay.

Miss on any one—especially speed—and even a winning stock prediction can turn into a losing trade.

This is why many professional traders prefer selling options (collecting premium) or using spreads to mitigate decay. Buyers face an uphill battle against time itself.

Key Takeaways for Option Traders

Always factor in implied volatility and remaining time when buying—high IV can inflate premiums, making the required move even larger.

Shorter-dated options have faster decay but cheaper premiums; longer-dated give more time but cost more upfront.

If you're directionally convicted and want leverage, consider whether the potential reward justifies the decay risk.

Paper trade or backtest scenarios to see how different price paths affect outcomes.

Options offer incredible leverage and opportunity, but they come with built-in hurdles that stocks don't have. Understanding time decay is one of the biggest edges you can develop.

Disclaimer: This post is for educational purposes only and is not financial advice. Options trading involves significant risk of loss. Consult a professional advisor and trade only with capital you can afford to lose.